In a nutshell

The conflict has struck a region already grappling with deep structural weaknesses: weak productivity, underperforming labour markets, limited job creation and heavy dependence on hydrocarbons; governments have increasingly been turning to industrial policy.

The MENAAP region is distinctive in how industrial policies are implemented – often through quasi-public institutions such as state-owned enterprises and sovereign wealth funds, rather than solely through ministries and formal policy announcements.

Industrial policy is most effective when the underlying causes of economic difficulties relate to market failures; by contrast, when weak governance, macroeconomic instability or political capture are the deeper constraints, it is unlikely to deliver lasting results.

On 28 February 2026, conflict erupted in the Middle East, sending shockwaves across the region and the world. The World Bank’s latest MENAAP Economic Update – encompassing the Middle East, North Africa, Afghanistan and Pakistan – examines the effects of the conflict on the global and regional economy, mapping out the key transmission channels.

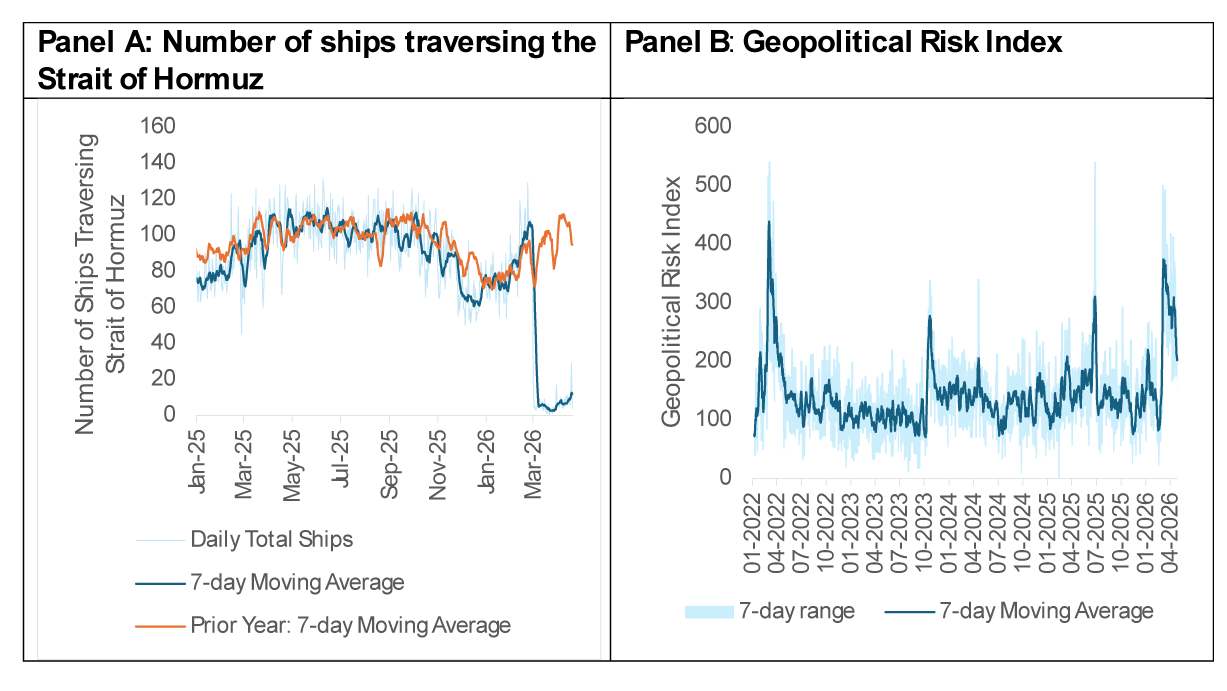

The outbreak of conflict has tested the resilience of the global economy. The Geopolitical Risk Index (Caldara and Iacoviello 2022) spiked to its highest daily reading since 2003 (see Figure 1, Panel B), and the effective closure of the Strait of Hormuz – one of the world’s most consequential maritime chokepoints (IEA 2022) – has dealt a major blow to global oil supply. Maritime traffic near the strait has come to a near-standstill (see Figure 1 Panel A), and oil and gas prices have risen by about 40% between 27 February and 22 April.

Figure 1: The disruption of the Strait of Hormuz and geopolitical uncertainty

The most severe and immediate economic consequences will be felt within the MENAAP region itself, shaped by two principal factors: proximity to the conflict; and exposure to the economic channels it has disrupted.

Iran and Lebanon have experienced mounting loss of life, mass displacement, destruction of infrastructure and severe economic disruptions. Both countries entered the conflict from positions of significant economic vulnerability.

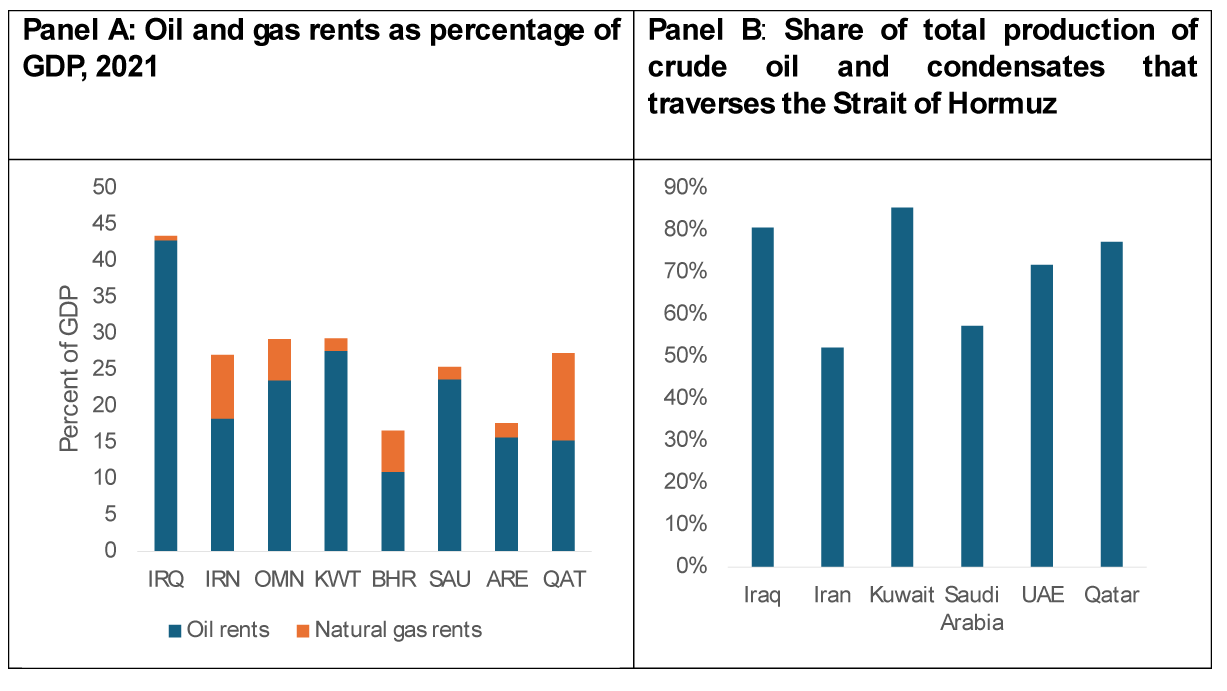

Other economies at the epicentre – Bahrain, Iraq, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates (UAE) – are heavily dependent on hydrocarbon exports (see Figure 2, Panel A), and the damage to their oil and gas production infrastructure and the closure of the Strait of Hormuz disrupts their primary export route to world markets (see Figure 2 Panel B).

Figure 2: Oil dependence and alternative export routes

Further from the frontlines, economies such as Egypt, Jordan and Pakistan face indirect but potentially significant spillovers through elevated hydrocarbon prices, energy shortages, reduced tourism and declining remittances from the Gulf. For many of these countries, the conflict arrives at a moment of pre-existing vulnerabilities, including heavy dependence on Gulf remittances or high sovereign debt paired with persistent fiscal deficits.

As a result, World Bank forecasts have been revised sharply downward. Real GDP growth for the region (excluding Iran) in 2026 is now projected at 1.8%, more than halved from the January forecast of 4%.

For the Gulf Cooperation Council (GCC) countries, growth is forecast at 1.3%, down from 4.2%. Iraq, Kuwait and Qatar are projected to contract by 8.6%, 6.4% and 5.7%, respectively (World Bank 2026a). Growth expectations for oil importers remain relatively unchanged, while forecasts for oil exporters outside the Gulf – such as Algeria and Libya – have edged upward.

Industrial policy

The conflict has struck a region already grappling with deep structural weaknesses. MENAAP economies share a difficult combination of challenges — weak productivity, underperforming labour markets, limited job creation and heavy dependence on hydrocarbons. To address these, governments are increasingly turning to industrial policy.

Industrial policy – which can be defined as government actions expected to increase strategic business activity (Fernandes and Reed 2026) – has gained prominence globally and across MENAAP. The strategic nature of industrial policy refers to the fact that it differentially benefits one sector. For example, a pillar of industrial policy for Morocco’s automotive sector is the specialised training programmes that it offers to create the types of skilled workers needed by the industry.

Industrial policy is often understood differently by economists and policymakers, but these perspectives are not disjoint. Economists rationalise industrial policy as a response to market failures, where private markets under-provide activities with high social returns, while policymakers frame it around concrete challenges – weak job creation, low productivity, limited diversification or environmental vulnerability.

Some of these challenges stem from market failures, such as coordination failures or underinvestment in worker training, while others reflect deeper institutional weaknesses or governance failures. Industrial policy is most effective when the underlying causes relate to market failures; by contrast, when weak governance, macroeconomic instability or political capture are the deeper constraints, it is unlikely to deliver lasting results.

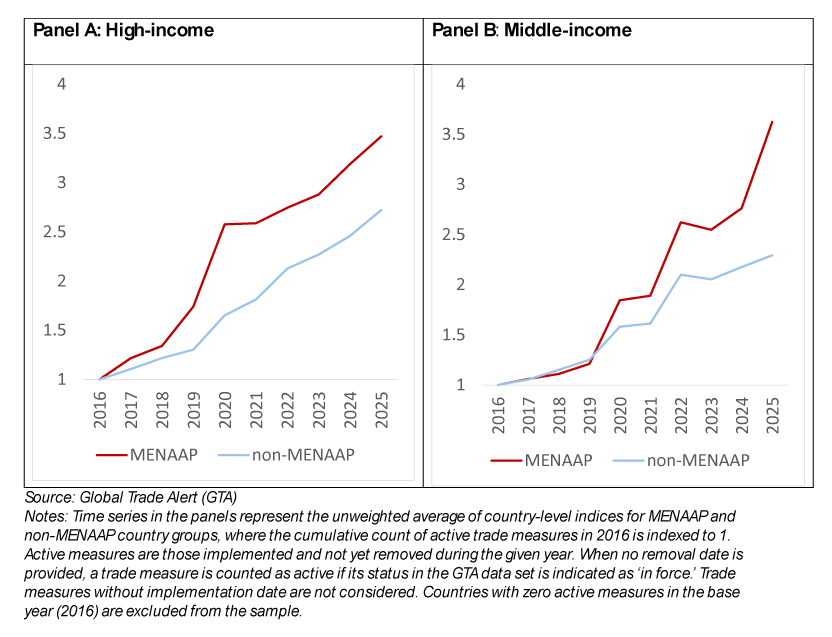

Over the past decade, such policies, measured by official announcements, have increased threefold in the region. A review of 19 national development plans reveals a striking degree of common purpose: unemployment is identified as a key challenge in 15 plans, job creation appears as an objective in all 19 and human capital development in 18. Economic diversification also features prominently.

The region is highly heterogeneous. Differences in fiscal space, institutional capacity and exposure to shocks determine which tools countries can realistically deploy. GCC economies rely more heavily on subsidies, while developing countries in the region make greater use of import-related policies that are less fiscally demanding.

Figure 3: Number of new industrial policies ‘in force’ (indexed to 2016)

MENAAP is also distinctive in how industrial policies are implemented – often through quasi-public institutions such as state-owned enterprises and sovereign wealth funds (SWFs), rather than solely through ministries and formal policy announcements.

SWFs in high-income MENAAP economies are among the largest in the world relative to GDP, and they are investing domestically in ways increasingly consistent with industrial policy. In the UAE, SWFs manage assets equivalent to roughly 460% of GDP, and the share of domestic assets under management of Saudi Arabia’s Public Investment Fund increased from 47% to 79% between 2020 and 2024.

The economic update presents four case studies – the digital ecosystem in Dubai; tourism in Egypt; the automotive industry in Morocco; and the soccer ball cluster in Pakistan – which highlight the heterogeneity in industrial policy experiences.

But all reforms – including industrial policies – depend on peace. Conflict is ‘development in reverse’: it costs lives and can destroy in weeks what takes generations to build. Seven years after the onset of conflict, per capita incomes in affected countries are about 45% lower than they would have been otherwise – equivalent to losing roughly 35 years of development (Gatti et al. 2024). The peace dividend for MENAAP is substantial, forming a much-needed foundation for long-term prosperity.

References and further reading

Caldara, D., and M. Iacoviello. 2022. “Measuring Geopolitical Risk.” American Economic Review 112: 1194–225. https://doi.org/10.1257/aer.20191823.

Fernandes, Ana Margarida, and Tristan Reed. 2026. Industrial Policy for Development: Approaches in the 21st Century. Policy Research Reports. World Bank. https://doi.org/10.1596/978-1-4648-2276-6.

Gatti, Roberta; Torres, Jesica; Elmallakh, Nelly; Mele, Gianluca; Faurès, Diego; Mousa, Mennatallah Emam; Suvanov, Ilias. 2024. Growth in the Middle East and North Africa. Middle East and North Africa Economic Update, October 2024. © World Bank. http://hdl.handle.net/10986/42000 License: CC BY 3.0 IGO.

IEA (International Energy Agency). 2022. Oil Market Report—March 2022. IEA. https://www.iea.org/reports/oil-market-report-march-2022.

World Bank. 2026a. Macro Poverty Outlook: Country-by-country Analysis and Projections for the Developing World, Spring Meetings 2025. © World Bank. http://hdl.handle.net/10986/43251 License: CC BY-NC 3.0 IGO.

World Bank. 2026b. Challenges of Conflict and Industrial Policy for Development. Middle East, North Africa, Afghanistan & Pakistan Economic Update (April 2026). World Bank. doi: 10.1596/978-1-4648-2328-2. License: Creative Commons Attribution CC BY 3.0 IGO