In a nutshell

The current double crisis shows that oil wealth is only temporary. The Kuwaiti people need to make a transition to earning their living from productive activities rather than depending on jobs supported by the rents from oil.

In the current social contract, the government, and the majority of parliamentarians, are keen for the economy to stay in public hands in order to be able to control the patronage from the distribution of rents that ensures political stability and regime sustainability.

A comprehensive set of reforms is necessary to unshackle Kuwait’s economy, including ending the public employment guarantee scheme and the non-contributory nature of the welfare state; and strengthening the framework of accountability for public procurement, tenders and bidding processes to ensure market competition.

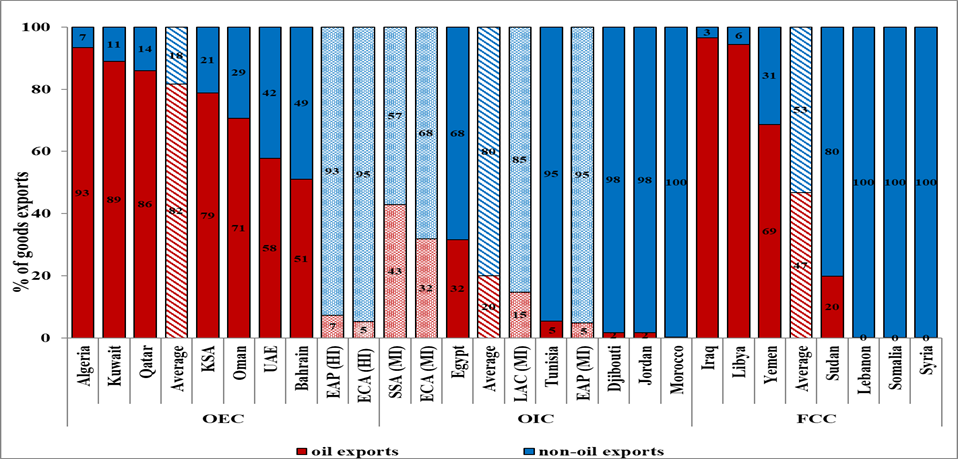

Kuwait is a small high-income country. With a population of just over four million, it is the third richest oil-exporting country (OEC) after Qatar and the United Arab Emirates. Its economy is almost entirely dependent on oil. Oil accounts for 90% of all merchandise exports and over one-third (37%) of the country’s GDP in 2019 (Figure 1).

In terms of the labour market, services dominate the economy. Almost three-quarters (74%) of employment is in services and one quarter is in industry, with just 2% in the tiny agricultural sector. There is a substantial government sector, accounting for about two-thirds of all economic activity, leaving a small share for the private sector.

Figure 1: Oil and non-oil exports’ share in total merchandise exports by region (2019)

Source: Author’s calculations based on WITS database. Notes: *selected classification HS 1988/92. *Regional averages are calculated as the weighted average of the values for the indicated countries. The weights are population based.

The nature of the Kuwaiti economy affects the characteristics of micro, small and medium-sized enterprises (MSMEs) and the way in which the sector has been affected by the Covid-19 crisis and the ensuing oil price shock.

The first consequence of the economy’s oil dependence is the low relative share of MSMEs in economic activity. Kuwait has one of the lowest MSME densities in the region: there are just over 12 enterprises per 1,000 people, which is almost just half the average in the Arab region as a whole (22.7), and a third that in oil importing countries (OIC). Comparator regions such as high-income Europe and Central Asia and East Asia and the Pacific have an MSME density of around five times that of Kuwait.

The MSME sector contributes just 3% of GDP, compared with 50% in high-income economies. It accounts for just 23% in Kuwait’s total workforce, which is half the average in high-income and emerging economies. The sector accounts for the majority of foreign and migrant workers in the country.

A survey by Bensirri Public Relations Kuwait shows that as in other countries, small enterprises tend to be young enterprises. About 60% of micro enterprises (those with fewer than ten workers) are young (four years old or younger) and the same proportion of large firms (those with more than 100 workers) are very old (over 15 years old). As discussed below, the policy environment in Kuwait does not encourage these small enterprises to grow.

The double shock: Covid-19 and oil prices

In 2014, oil prices fell to levels not seen for nearly 15 years, falling from over US$110 a barrel at the start of the year to a low of US$38 by February 2016. There had been a modest recovery before Covid-19, but following the outbreak, in the first part of 2020, oil prices fell to a low of less than US$20 a barrel in April 2020. In that month, oil was selling at negative prices in some markets for the first time in history.

This double crisis of Covid-19 and the oil price shock has disproportionately hit the Kuwaiti MSME sector. The Bensirri Public Relations Kuwait Covid-19 Business Impact Survey covered 536 formal sector enterprises, all of which were profitable before the crisis. As a result of the crisis, half of all surveyed enterprises (45%) have suspended or shut down their businesses. But while 60% of all microenterprises and 70% of all small enterprises have shut down their operations, only 23 % of large enterprises have done so.

Moreover, MSMEs face more grave cash flow challenges than do large enterprises: 27%, 35% and 24% of the micro, small and medium-sized enterprises, respectively, face challenges in access to finance and funding capital compared with just 19% of large enterprises. Thus, larger and older enterprises have not been as severely affected as the smaller, more private sector-oriented MSMEs.

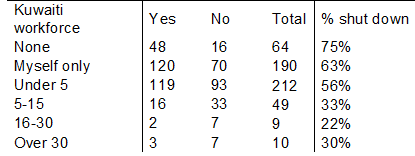

A striking finding of the survey is that the fewer Kuwaiti employees an enterprise has, the more likely it is to have suspended its operations or shut down in response to the crisis (see Table 1), indicating that they have been receiving minimal support.

Table 1: Incidence of shutdown or suspension by Kuwaiti workforce

Source: Author’s calculations based on the Bensirri PR Kuwait Covid-19 Business Impact Survey (2020).

Did the MSME sector receive government support proportionate to the damage it suffered?

Like many governments around the world, the Kuwaiti government introduced a range of monetary and fiscal measures. In addition, the government implemented rescue measures specifically directed at SMEs, such as:

- Reducing their risk rating from 75% to 25%.

- Providing them with concessional long-term loans with joint financing from local banks and the Kuwait National Fund for the Promotion and Development of SMEs (KNFS).

- Postponing due instalments to the KNFS and the Industrial Bank of Kuwait.

- Postponing collection of social security contributions from business owners in the private and partially state-owned oil sectors for six months.

But most MSMEs are unaware of these measures. Over 60% of micro, 56% of small, and half of all medium-sized enterprises either have entirely no knowledge of the package or are not familiar with the details. In comparison, 75% of the large enterprises are either somewhat familiar or very familiar with the package. This suggests that support is going mainly to larger businesses, which helps to explain why larger firms have been less likely to shut down than smaller ones.

One reason for this bias in the distribution of assistance is the eligibility requirement to apply for crisis loans requiring SMEs to comply with the ‘Kuwaitisation’ policy quota. This policy reinforces the muted entrepreneurial incentives that afford excessive protection from competition to Kuwaiti national entrepreneurs, which serve to defeat the purpose of the government’s decades long entrepreneurial assistance.

Structural issues in Kuwaiti development policy: Dutch disease Kuwaiti-style

Kuwait suffers from a particular form of Dutch Disease, the phenomenon named after the impact of gas discoveries in the North Sea on the Dutch economy in which natural resource booms exerted adverse effects on other sectors of the economy. Competitiveness of other sectors is reduced as are incentives in growing the tax base, and revenues may be used to support unsustainable investments including expanding the public sector, as is clearly the case in Kuwait.

In Kuwait, this problem has partly manifested itself in the well-known problems of school quality, higher education standards and lack of vocational training, which have pushed the national labour force out of scientific and technical occupations and out of the private sector altogether. But there are a number of reasons other than Dutch disease (although sometimes also related to it), which account for the structural vulnerabilities of the Kuwaiti economy.

First, there is the nature of the Kuwaiti welfare state and the generous availability of lifetime secure government employment for all Kuwaiti nationals. Both of these factors dampen the incentives for individuals either to engage in entrepreneurial and risky business activities or to seek additional private sector employment.

Kuwaiti nationals account for less than 20% of overall employment and are predominantly concentrated in the government and public sectors. In the current Kuwaiti social contract (El-Haddad, 2020), the government pays for subsidised basic food, free education and health care, free housing and goes as far as making overseas provisions of medical treatment and education. Generous allowances for wives and children are also standard.

Second, another break on private sector development is that for decades foreigners were not allowed to have sole ownership of companies in Kuwait, although this changed in 2016. Thus, Kuwaiti private entrepreneurs are also protected from foreign competition by law. But this does not mean they are necessarily entrepreneurial. Rather, as any foreign business had to have a Kuwaiti co-owner, they can behave as silent partner, having no active role in the running of the business.

In fact, Kuwait’s total entrepreneurial activity per 100 people at 2% (known as the total entrepreneurial activity indicator) is less than one-fifth of the world average of 11%. It is far below what is expected of a country at its income level. The persistence of such policies and practices will only stifle the growth of fledgling enterprises especially MSMEs, which has serious implications for long-term efficiency as MSMEs are typically the main sources of innovation, job creation and growth.

Third, the Kuwaiti government monopolises a range of sectors: from oil to aviation, gas stations, entertainment parks and even movie theatres (Ahmed and Al-Owaihan, 2015). These sectors are not natural monopolies, and so there is no rationale for them being under public ownership. In the current social contract, the government, and the majority of parliamentarians, are keen for a large part of the economy to stay under state control in order to be able to control patronage from the distribution of rents that ensures political stability and regime sustainability.

Similarly, franchising is monopolised by a few big franchisees. Franchising in countries all over the world is an opportunity for MSMEs to thrive. In Kuwait, multiple franchises that cover all of Kuwait, and beyond, are exclusive to a single franchisee. This is not the usual model for companies such as McDonalds, Burger King, Starbucks, The Body Shop and Toyota. Powerful businesspeople own the multiple outlets for more than one brand name. Favouritism is the obvious culprit. All these government-backed monopolies are barriers to entry to potentially successful MSMEs.

A new policy agenda towards a new social contract

The current double crisis shows that the oil wealth is only temporary. The Kuwaiti people need to make a transition to earning their living from productive activities rather than depend on jobs supported by the rents from oil. Kuwait cannot prosper in the long run without competition and diversification. The needed reforms imply a new social contract in which benefits distributed to the population by government are substantially reduced.

The current crises present a chance for Kuwait to renegotiate the social contract without igniting social unrest (Loewe et al, 2019). It is thus an opportunity to adopt the necessary reforms to make its economy more dynamic and to encourage MSME and job creation post-crisis.

A comprehensive set of reforms is necessary to unshackle Kuwait’s economy. Such reforms should include:

- Ending the public employment guarantee scheme and the non-contributory nature of its welfare state to provide incentives for Kuwaiti nationals to engage in the economy.

- Strengthening the framework of accountability for public procurement, tenders and bidding processes in order to ensure market competition. For example, it is necessary to ensure the actual implementation of the recently promulgated new Public Tenders Law, which governs the award of public investment projects, an essential step to achieving more competition.

- Liberalising to lift legal monopoly restrictions and privatising to insulate companies from political interference in their daily management.

- For sectors that will remain in public hands, implementing public sector reform such as the incorporation of public companies, to enhance public businesses’ managerial and financial autonomy. Autonomy will harden the ‘soft’ budget constraint that firms face when they know government will make up any shortfall between income and expenditure, and so discipline government-dependent public businesses. If such discipline is not achieved, failing enterprises are forced to exit the market with no chance for bail out.

- Ensuring better public financial management, which will introduce similar discipline into public finances and prepare the government to manage future shocks.

- Implementing reforms to ensure the transparency of the use of the country’s oil wealth. Here important governance reforms include joining the Extractive Industries Transparency Initiative (EITI), enacting oil and gas sector transparency laws, including requiring the government and companies to publish oil contracts and running public consultations on the management of sovereign wealth funds.

The combined effect of these reforms together will help support a new environment that opens up chances for greater diversification and the gradual retreat of the Kuwaiti non-contributory welfare state and state-sponsored employment. This will allow MSMEs to thrive, the Kuwaiti people to engage in productive private employment and so bolster the long-run development prospects of the country.

Further reading

Ahmed, Ahmed Abdel Rahman, and Abdullah Al-Owaihan (2015) ‘Kuwait SMEs: Size, obstacles and suggested remedies’, International Journal of Managerial Studies and Research 3(8): 7-14.

El-Haddad, Amirah (2020) ‘Redefining the social contract in the wake of the Arab Spring: the experiences of Egypt, Morocco and Tunisia’, World Development 127.

Loewe, Markus, Bernhard Trautner and Tina Zintl (2019) ‘The social contract: an analytical tool for countries in the Middle East and North Africa (MENA) and beyond’, German Development Institute/Deutsches Institut für Entwicklungspolitik (DIE) Briefing Paper 17/2019.