In a nutshell

Rising sea levels are the biggest climate change threat to the Arab region, with Egypt, Tunisia, Qatar and the UAE likely to suffer most; other impacts include a shortening of the growing season, spread of infectious diseases and loss of already limited water supplies.

Recent advances in technology have allowed for the rapid expansion of solar and wind generation capacity; these new energy sources are proving to be effective substitutes for fossil fuel-based electricity, even in the most fossil fuel-endowed countries of the region.

Renewable energy can bring about a major change in the labour market of the region, supporting the creation of a large stream of new jobs, reducing high unemployment rates and offering better opportunities for women and young people.

The Earth’s climate is warming, a trend that has accelerated over the last three decades. The ten warmest years on record have all occurred since 1998, with 2023 being ranked as the warmest on record. This could soon be replaced by 2024.

Warmer and moisture-laden air is more turbulent and tends to produce more violent weather patterns. These phenomena have contributed to the increasing frequency and severity of extreme weather events, such as floods, thunderstorms, droughts and heat waves. There has been a steady increase in devastating disasters of this kind across the globe.

The United Nations Disaster Risk Reduction Program has found that over the last few decades, 76% of all disasters were associated with climate and/or weather conditions such as heat waves, freezing or winter storms, wild fires, droughts, tropical storms, hail, tornados, flash floods, river floods and landslides. These events accounted for 45% of the deaths and 79% of the economic losses caused by natural hazards.

Economic impacts of climate change

The physical impacts of climate change translate into significant public and private costs, in aggregate and across numerous sectors. The exposure and vulnerability of people and physical and natural assets to climate change are dynamic, varying across temporal and spatial scales. They are also heavily influenced by economic, social, geographical, demographic, cultural, institutional, governance and environmental factors.

Quantifying the economic impacts of climate change is essential for an informed policy debate about the urgency and choice of actions to mitigate the most severe effects and to increase the resilience of communities to the aftermath. There is little research done on this for the Middle East and North Africa (MENA) despite an increasing number of extreme climatic events even in countries that had never been exposed previously to them – for example, flash floods in Dubai and Jeddah.

Early work on the economics of climate change focused largely on defining the scope of social and economic impacts. Estimates were generally at the global and large regional levels, and they were aimed particularly at informing international negotiations on climate change. But there has been little research to assess the economic impacts of climate change and extreme weather events at the country level or to assess the costs of inaction even at the regional level.

In general, economic losses are critically dependent on the frequency and severity of extreme events. Risk relates to the probability of the occurrence of an event and the magnitude of the consequences of its occurrence. It can be quantified in formal ways using probability density functions of the variables and forecasts. These studies are necessary and could easily be done for the MENA region. They will define the magnitudes of expected costs and could guide policies to mitigate their negative effects.

The expectation at this time is that world temperatures may rise by between 1.1 and 6.4 degrees centigrade during this century relative to the period 1980-99, depending on the emissions scenario realised. Sea levels are expected to rise by 18-59 centimetres by 2100, with thermal expansions of oceans being the single most significant contributor.

There is greater than 90% confidence that there will be frequent warm spells, heat waves, high evaporation, intense precipitation and severe weather events. And there is greater than 66% confidence that there will be an increase in droughts, tropical cyclones, extreme high tides and storm surges.

Vulnerability of the Arab region to climate change

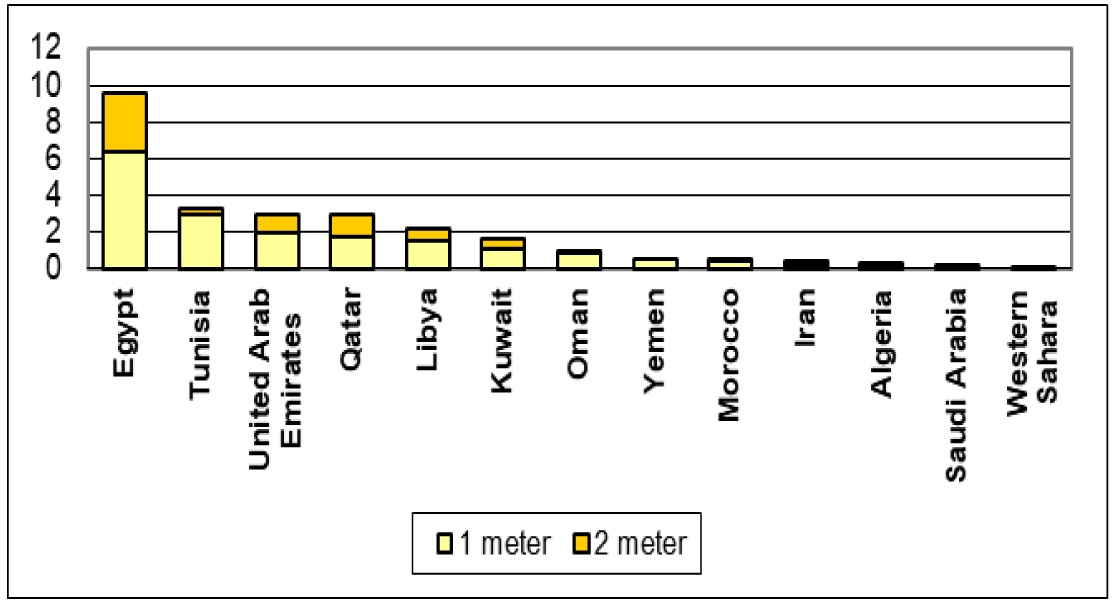

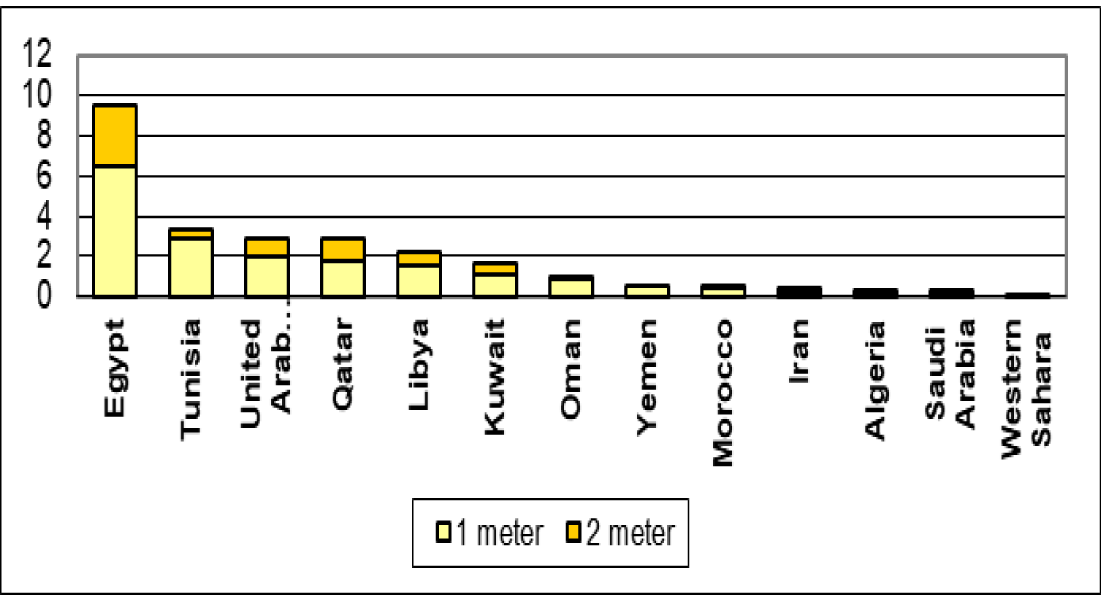

The Arab region is very fragile and highly vulnerable to climate change disasters. It is estimated that a one metre rise in sea levels will affect 3.2% of the population (see Figure 1) and 1.49% of GDP (see Figure 2). These percentages exceed all other regional impacts. Egypt, Tunisia, Qatar and the UAE will suffer most from any sea level rise. Other climate change impacts include a shortening of the growing season, spread of infectious diseases and loss of already limited water supplies.

Figure 1: Projected impacts of sea level rise – percentage of the population affected

Figure 2: Projected impacts of sea level rise – percentage of GDP affected

There is a fundamental need for a better understanding of the range of possible climate change outcomes at the Arab region level, at the country level within the region and in some particularly vulnerable regions (such as the Delta region in Egypt and the Gulf states)

In particular, it is vital to explore the impacts of climate change on:

- Infrastructure – transport, water supply, health facilities, etc.

- Agriculture and food production – food security in the region is particularly precarious.

- Water – almost all countries in the region are below the water poverty level.

- Health, including climate-prone diseases.

- Energy and stranded assets.

- Productivity declines as heat waves accelerate.

- Adaptation programmes and projects.

- Financing damages and losses due to climate change.

Time to move away from fossil fuels

The scientific community in general and climate scientists in particular are convinced that carbon emissions from the use of fossil fuels are the main factors driving these climate change developments. It is now a well-established scientific fact that the extraction and use of fossil fuels at the same rates and volumes as the world used in the recent past are no longer consistent with sustainable life.

The case against ‘business-as-usual’ use of fossil fuels and their contributions to climate change is typically argued on moral and environmental grounds. But there are sufficient economic reasons to suggest that investing in fossil fuels exposes the investors to higher risks and lower returns than investing in renewable energy. Better yet, the development of renewable energy and phasing out of fossil fuel extraction, production and transport hold the promise of generating more and better jobs, higher incomes and better social outcomes.

A 2015 study argued that an estimated one-third of oil reserves, half of gas reserves and more than 80% of known coal reserves must remain unburned in order to meet global temperature targets under the Paris Agreement (McGlade and Ekins, 2015). The development of alternative or green energy has increasingly been seen as one critical strategy to meet the expected world demand for energy that is sustainable, clean and environmentally friendly and which can generate good paying jobs and social inclusion.

The Arab region has the lowest cost of extraction of fossil fuels and the largest deposits of these resources. Arab oil and gas producers and exporters are likely to make profits even at very low oil and gas prices. But they are vulnerable to great losses if and when these assets become stranded assets. Perhaps more serious is the heavy dependence of these countries on oil rents to finance their development needs given the limited diversification of their production and exports.

But this is not the only challenge: the region can divert its huge energy reserves to other uses other than as fuels, such as the production of fertilisers, pharmaceuticals, plastics, furniture and a host of other products.

More importantly, the region is endowed with the world’s highest levels of solar irradiation. It is also home to huge empty spaces and deserts that can support the production of solar and wind energy at levels which can power not only the Arab region but also many other parts of the world. Indeed, Morocco is already planning to supply electricity to the UK; and Saudi Arabia and the UAE are considering exports of renewable energy to other Arab countries and to India and many other faraway locations.

The potential of renewable energy

Over the past few decades, the world has witnessed a significant shift toward renewable energy sources. For example, one study finds that generating 35% of electricity using wind and solar in the west of the United States would reduce carbon emissions by 25-45% (NREL, 2017).

The widespread adoption of renewable energy technologies – such as solar, wind, biomass, green hydrogen and hydro – has not only helped to reduce emissions of the greenhouse gases that cause climate change; it has also had a profound impact on employment, incomes and social outcomes. The costs of renewable energy production have fallen dramatically, technologies have become more efficient and solutions for integrating renewables into electric grids have advanced measurably.

A recent ERF study explores the employment impacts of renewable energy, particularly how it is changing the labour market in the MENA region (Kubursi and Abou-Ali, 2024). The research finds that renewable energy can support the creation of a large stream of new jobs, reduce high unemployment rates and offer better opportunities for women and young people.

The renewable energy sector has recently emerged as a major global employer, creating new job opportunities and offering higher-quality jobs compared with the traditional energy sector. In fact, every dollar of investment in renewables creates three times more jobs than in the fossil fuel industry (Guterres, 2021).

The IEA estimates that the transition toward net-zero emissions will lead to an overall increase in global energy sector jobs (Cozzi and Motherway, 2021). The report notes that while about five million jobs in fossil fuel production could be lost by 2030, an estimated 14 million new jobs would be created in green energy.

There are several ways to generate electricity. For over a century, fossil fuels have been the main source of power generation. Although, important sources for the generation of electricity, both hydroelectric and nuclear facilities have never truly competed with coal and natural gas for total generation capacity.

But recent advances in technology have allowed for the rapid expansion of solar and wind generation capacity and these new sources are proving to be effective substitutes to fossil fuel-based electricity, even in the most fossil fuel-endowed countries of the MENA region. Embracing clean electricity is becoming the new dominant source of green energy, and it carries the promise of restructuring the world economy and its prospects.

Further reading

Cozzi, L, and B Motherway (2021) ‘The importance of focusing on jobs and fairness in clean energy transitions’, IEA.

Guterres, A (2021) ‘Opening remarks to High-level Dialogue on Energy’, United Nations.

Kubursi, A, and H Abou-Ali (2024) ‘Potential Employment Generation Capacity of Renewable Energy in MENA’, ERF Policy Research Report No. 47.

McGlade, C, and P Ekins (2015) ‘The geographical distribution of fossil fuels unused when limiting global warming to 2°C’, Nature 517: 187-90.

NREL (2017) ‘Western Wind and Solar Integration Study’.

The work has benefited from the comments of the Technical Experts Editorial Board (TEEB) of the Arab Development Portal (ADP) and from a financial grant provided by the AFESD and ADP partnership. The contents and recommendations do not necessarily reflect the views of the AFESD (on behalf of the Arab Coordination Group) nor the ERF.