In a nutshell

The benefits of workplace adaptation during Covid-19 were primarily realised by firms in industries with high capacity for remote work; firms in industries with low capacity for remote work were more likely to benefit from process adaptation and trade credit.

The multiplicity and suddenness of crises require that emergency business support systems need to be thought out well in advance; they should be dynamic and adapted to the different phases of a crisis – and they should take account of its first and higher-order effects.

In the context of a short and strict lockdown, once it is brought to an end, the government should redirect its financial support measures away from firms exposed to the labour input shock and towards firms exposed to the demand and intermediate input shock.

While the world has effectively succeeded in containing the Covid-19 pandemic, it continues to grapple with a myriad of crises. From conflicts to natural disasters, our societies and economies remain under immense pressure. The MENA region, in particular, is one of the most vulnerable to both geopolitical tensions and climate change.

Understanding economic shocks, such as the lockdown policy response to the pandemic, and how firms adapt to them is crucial for mitigating their impact, accelerating recovery and handling other shocks such as natural disasters or conflicts. These events can cripple supply chains and erode consumer demand, leaving businesses vulnerable. The Covid-19 crisis offers a large-scale natural experiment of various initial and higher-order supply and demand shocks.

In a recent study (Le et al, 2024) we draw lessons from the pandemic to establish a framework for analysing responses to future shocks. First, we quantify the impact of the crisis on small and medium-sized enterprises (SMEs) and explore the main channels through which they were affected. Next, we identify which types of SMEs performed better during and after the crisis. Finally, we aim to understand which firms adapted most effectively and how they did so.

We focus on SMEs as they represent around 95% of registered firms in the MENA region and employ half the population. They are also probably more vulnerable than larger firms due to their lower access to credit and public policy support.

Shortage of labour, intermediate inputs and demand

The three channels through which the pandemic affected SMEs are the labour input shock, the demand shock and the intermediate input shock.

The labour input shock stemmed from business closures and social distancing measures. The shortage of intermediate inputs resulted from reduced labour in intermediate-input industries and the difficulties of transport, particularly for imported intermediate inputs. The demand shock arose from shifts in household spending patterns across sectors and time.

Our key variables are the variation of these shocks across industries.

Firm adaptation

Technological adaptation, credit constraints and firm heterogeneity can amplify or mitigate the effects of the supply and demand shocks. Technological adaptation and credit constraints are proxied respectively by indices of the extent to which an industry has capacity for remote work, and an industry’s dependence on external finance. Firm heterogeneity is considered by size, export status and ownership (domestic or foreign).

To investigate further how SMEs adapted in terms of technology and finance, we examine three kinds of adaptation implemented by firms: workplace adaptation; process adaptation; and the use of trade credit.

Impact and persistence of the shocks

The supply and demand impacts of Covid-19 and the lockdown were aggregate shocks, but their effects were notably heterogeneous across industries. We deploy these sectoral variations of shocks to investigate their effects on Tunisian SMEs, using data from the census of all registered (formal) firms in the country.

We find that SME performance in 2020 was heavily affected by a combination of labour input, demand and intermediate input shocks. We also find that exporting firms performed better in facing the three types of shocks, while foreign firms performed better in response to the labour input and demand shocks only.

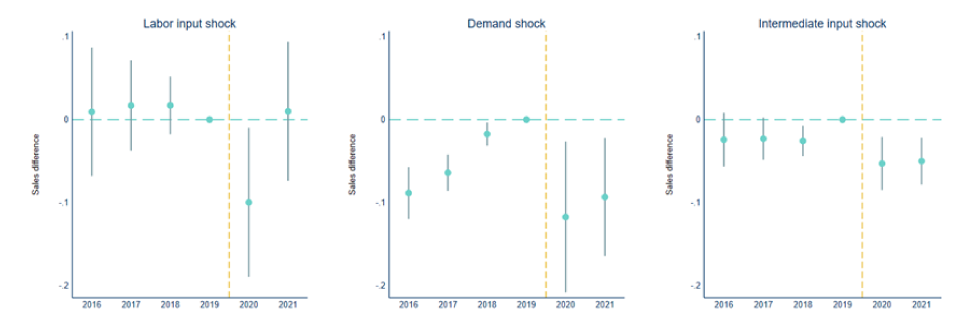

Not surprisingly, firms in sectors with higher external financial dependence were more affected by the demand shock. In 2021, the effect of the demand and intermediate input shocks persisted at a relatively similar negative level, while the impact of the labour input and demand shocks were no longer significant (see Figure 1).

Figure 1: Differences in log of sales of firms (2016-21)

Our results suggest that in the context of a short and strict lockdown, once it is brought to an end, the government should redirect its financial support measures away from firms exposed to the labour input shock and towards firms exposed to the demand and intermediate input shock.

Capability driven adaptation

To study firms’ coping strategies and the determinants of firm adaptations, we launched a representative survey conducted in person by our team in the summer of 2020. We evaluate the likelihood of firm adaptation to the three shocks conditionally on their characteristics.

We find that firms in non-essential industries, which were hit hardest by the lockdown, were less able to adapt than firms in essential industries during the first lockdown. The stringent and abrupt nature of the lockdown may have limited the ability of closed firms to respond effectively. Moreover, they may have encountered liquidity constraints, hindering their capacity to invest in adaptation strategies. In other words, firm adaptation seems to be driven more by capability than by necessity.

Furthermore, younger and larger firms were more likely to adopt process adaptation, while exporters and foreign-owned firms benefited from better access to trade credit and were more capable of adjusting their sales and production processes.

We then assess the impact of three adaptation strategies on firms’ resilience to the supply and demand shocks by incorporating them into estimates of the impact of the shocks on firm performance.

Our findings indicate that firm adaptations, particularly process adaptation and trade credit, were generally associated with better performance during the lockdown. Moreover, the benefits of workplace adaptation were primarily realised by firms in industries with high capacity for remote work. Conversely, firms in industries with low capacity for remote work were more likely to benefit from process adaptation and trade credit.

Trade credit’s positive impact was most pronounced in industries with significant external financing needs. Intriguingly, workplace adaptation also mitigated the negative effects of shocks for firms in industries with high external financial dependence. This suggests that while remote work adoption was industry-specific, it may not have been a costly adaptation for these firms.

Conclusion

Given the limited financial resources of governments, particularly after the Covid-19 crisis, support for firms needs to be as targeted as possible. The targeting needs to take account of the characteristics of the relevant firms.

The multiplicity and suddenness of crises require that emergency business support systems need to be thought out well in advance. They should be dynamic and adapted to the different phases of a crisis, and they should take account of its first and higher-order effects.

Our study gives some insights to prepare the reaction to future crises, particularly on firm adaptation. But it only deals with formal firms due to the absence of statistics on informal ones, while studies of Covid-19 often show that the informal sector was more affected by the pandemic.

This entails that the statistical system should cover the informal sector by launching surveys such as the Labor Market Panel Surveys that ERF has promoted in recent decades. Governments should also collaborate with the research community to develop monitoring and evaluation systems that can help to support a quick reaction when a crisis emerges.

Further reading

Krafft, Caroline, Ragui Assaad and Mohamed Ali Marouani (2021) ‘The Impact of COVID-19 on Middle Eastern and North African Labor Markets: A Focus on Micro, Small, and Medium Enterprises’, ERF Policy Brief No. 60.

Le, Min-Phuong, Lisa Chauvet and Mohamed Ali Marouani (2024) ‘The Great Lockdown and the Small Business: Impact, Channels and Adaptation to the Covid Pandemic’, World Development 182: 106673.